Has your business growth flattened or even decayed in your market, and no amount of marketing or sales seems to be able to help it? What do you do? Develop new solutions for this market? Try to enter adjacent markets? Here is a process that we have seen used successfully in a number of different technology companies to recharge growth in revenue and profits.

Start with re-examining the Mission and Vision of your company. Why does your company exist, and what would it look like in 5 years if it was more successful in fulfilling that Mission? Don’t accept some generic statement like “to increase shareholder value.” Your Mission statement should be unique to your company, and not apply just the same to General Motors, Apple Computer, or Mrs. Fields Cookies. What will you NOT do?

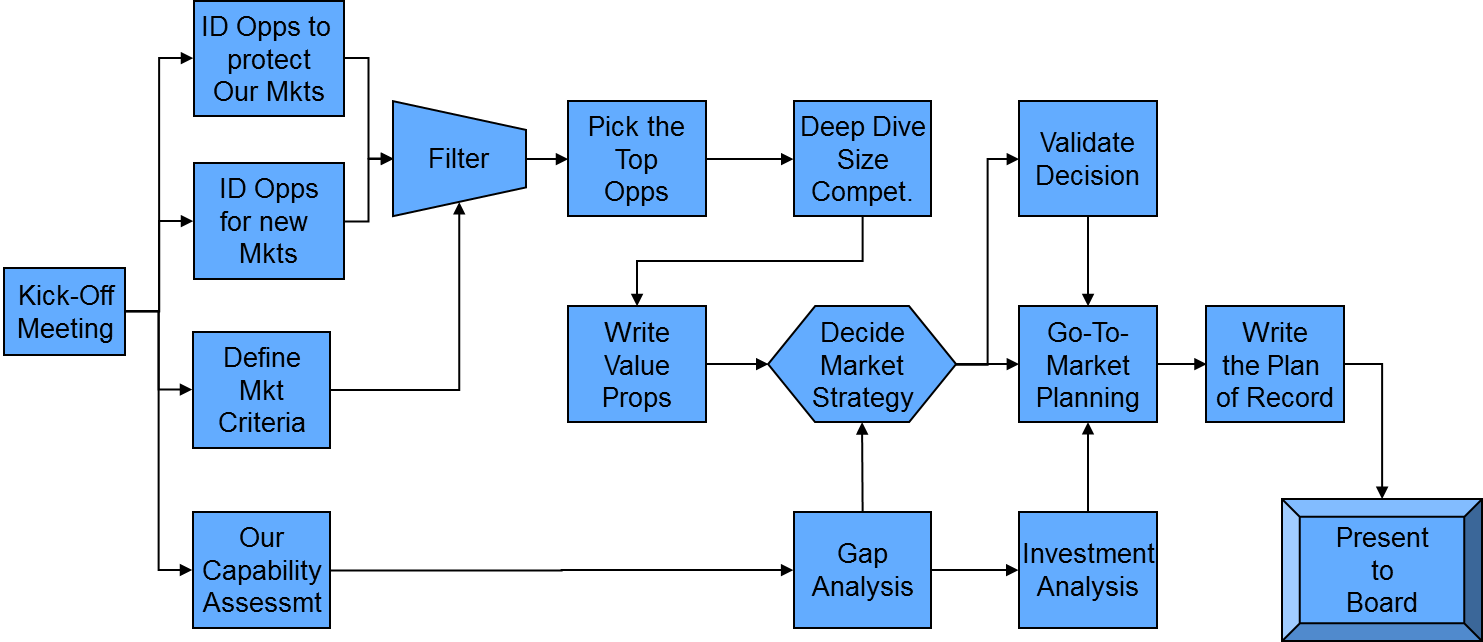

The Mission and Vision statements give you the framework to take the next steps, illustrated below:

Gather the Strategic Planning team to kick-off a Strategic Planning session. This team is usually composed of the Senior Executive Staff along with some company thought leaders and maybe a key outside partner or two. An expert facilitator (such as one from TrustedPeer.com) can really help focus the effort and move things along, but the CEO should be the main driver. Give yourselves enough time to develop a robust and validated plan – usually 2 to 4 months, depending upon people’s availability and the amount to market research undertaken.

The first four steps should be done in parallel:

- Identify what must be done to defend your current market share. The plan may involve developing new solutions, refreshing older ones, and adding marketing and service resources to provide increasing value and love to your customers.

- Identify opportunities to enter new or adjacent markets, where you don’t currently play. This exercise is challenging because the opportunities (and the work to find them) may seem endless. Fortunately, the Internet and search engines allow efficient ways of finding and researching many opportunities. Don’t be afraid to engage outside experts or buy professional reports in areas of potential interest. Don’t just look in the most obvious and familiar places – encourage creative thought and cast a wide net. And don’t just look at areas where you have a “core competency” (see the blog: Tenet #1 of Ten Tenets of Strategy: Your core competency is not your strategy). Needed core competencies can be acquired and unneeded ones can be divested. What is important is that the new opportunities optimally fulfill your Mission and Vision. For each opportunity identified, do a short SWOT and market sizing. Pick a person in the team to “champion” each one and write a brief business case.

- Define the market criteria for markets you may want to pursue. What are the Total Available Market (TAM) and Segmented Addressable Market (SAM) sizes that you need to see to make it worthwhile? What are the minimum revenues and margin you would consider? How fast should the total market be growing before you would consider it? What barriers to entry would keep you from entering it? How much are you willing to invest to enter a new market? These criteria will be your filter for subsequent steps.

Do a capability assessment: What are your company’s Core Capabilities? (Not your Core Competencies; see Tenet #2 of Ten Tenets of Strategy: Compete on Core Capabilities). We advise you to seek outside experts to help you figure out what you do that makes you successful in the first place. It’s a bit like medical self-diagnosis – too easy to be fooled by your own self biases.

By this time, you should have identified 20 or 30 or more possible opportunities to either protect and grow your existing markets or grow into new ones. Now it is time to filter and prioritize. Look at the brief business case for each of those opportunities and apply your market criteria to them. How does each one stack-up against the others? Prioritize and pick the top 5 to 10 candidates.

Have the “champions” for each of the top opportunities lead a “deep dive” market research effort and write a more detailed business case. Give them the time and resources to do a proper job so that the market size, potential share, achievable margins, etc. are reasonably accurate and validated. The business case should contain potential Value Propositions for your company: what customers will you serve, what pain or unmet needs are you addressing, and what would your solution need to add to have them choose it over other available solutions?

Prioritize the opportunities based on comparing these business cases, and on your “bandwidth” – your appetite and resources available for such initiatives. Most companies cannot attempt more than 3 or 4 new such initiatives at the same time. The winning initiatives will form the basis of your market strategy; make sure that the whole team buys into pursuing them.

Study how your market strategy matches your capability assessment: what are your strengths and gaps for entering these markets? What do you need to do to fill the gaps and strengthen your core capabilities? These factors are critical in deciding your market strategy.

Validate your decision through further market studies, and develop a detailed market strategy plan, including goals, timing, investment, resources needed and scenario planning. Decide what events or metrics might trigger a change in your plans. Discuss these plans and tweak them until every member of the team is satisfied that it is a plan with the highest probability for success. This plan becomes the Plan of Record.

Present the Plan of Record to the Board or Executive Committee for approval or modification.

Of course, this process or any other Strategic Planning process cannot guarantee that you will be successful. It needs to be followed by excellent execution, inspirational leadership, and a fair measure of good luck. But it does give you the best chance of success.

To book an expert session with Scott, go to Scott's page on TrustedPeer.